“Social media is the ultimate equalizer. It gives a voice and a platform to anyone willing to engage.” –Amy Jo Martin

This has not been a healthy market by any means. As I’ve noted numerous times, the vast majority of stocks have performed sub-par in what is otherwise supposed to be a strong year given pre-election dynamics. Small-caps, Europe, retailers and emerging markets have been whipsaw city.

The headline averages are being driven entirely by the “Magnificent Seven” of Apple (NASDAQ:AAPL), Microsoft (NASDAQ:MSFT), Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL), Amazon (NASDAQ:AMZN), Nvidia (NASDAQ:NVDA), Tesla (NASDAQ:TSLA) and Meta Platforms (NASDAQ:META). These will all at some point be sources of liquidity when volatility hits.

The weight of the biggest 5 stocks in the S&P 500 is at an all-time high.

You are being fooled by idiosyncratic risk.

WAKE UP. pic.twitter.com/2IHMUSQVBc

— Michael A. Gayed, CFA (@leadlagreport) September 7, 2023

Of the Magnificent Seven, I believe Meta is the most logical one to favor for now. Whether it’s the focus on artificial intelligence (AI), the expansion into Threads, or the company’s data-driven business model, I think the opportunities are substantial for Meta with a valuation multiple that is not too expensive.

Meta is the parent company of the world’s largest social networks, including Facebook, Instagram, Messenger and WhatsApp. With billions of daily active users, Meta’s platforms have fundamentally changed the way people interact, share information and conduct business. That information that Meta has on each of us — like it or not — is its edge.

Meta Platforms’ ‘Year of Efficiency’

Meta’s primary source of revenue is advertising. The company’s vast user base and sophisticated algorithms allow advertisers to target their ads based on various parameters including age, gender, location, interests and behaviors.

More than 98% of Meta’s revenue in the second quarter of 2023 came from advertising. This figure is projected to grow as Meta continues to meaningfully improve its ad targeting capabilities. As Threads grows and inevitably has advertising as a standalone network, and as the company’s AI initiatives expand, advertising revenue likely continues to benefit.

It’s more than just revenue, of course. This year has marked Meta’s “Year of Efficiency,” a strategic initiative focused on reducing costs and increasing operational efficiency. This initiative has resulted in significant margin expansion and improved bottom-line performance. One of the key strategies was aggressive cost-cutting. The company successfully streamlined its operations, resulting in improved operating margins.

Another critical aspect of theYear of Efficiency was its investment in AI. By leveraging advanced machine-learning algorithms, Meta has been able to improve its content recommendation systems, ad targeting capabilities and overall platform efficiency. AI will likely play a crucial role in Meta’s business strategy going forward.

The Bottom Line on META Stock

The stock has been on fire, and outperformed the S&P 500 meaningfully since the start of the year. The trend is still up for now, and it could reclaim its relative standing peak it had back in 2020. Relative to Nvidia and other AI plays, the stock is cheap and can continue to grab investor attention independent of short-to-intermediate-term volatility.

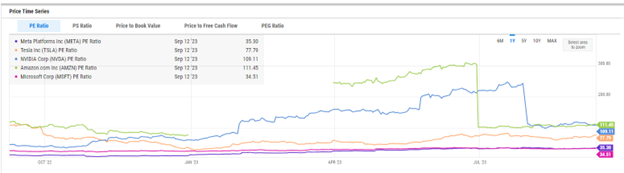

Despite the strong performance in META stock, Meta’s valuation remains attractive compared to its peers. As of September 2023, Meta’s stock was trading at a price-to-earnings (P/E) ratio of 35.6, which is a discount compared to other large-cap tech stocks. Against the other Magnificent Seven, it’s the second cheapest after Microsoft, which I’m also favorable on longer-term.

{kind=link}

The bottom line is that Meta will likely only become more of a dominant player in the global digital landscape. This is largely due to its strong growth prospects and attractive valuation. Its strategic focus on AI, expansion into Threads, and data-driven business model position the company well for future growth. Timing is everything, but I suspect META stock is one to unequivocally focus more time and energy on as opposed to just chase, as we’ve seen with stocks like NVDA.

The Lead-Lag Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by the Lead-Lag Report are independent of other services provided by Lead-Lag Publishing, LLC or its affiliates, and positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors and employees expressly disclaim all liability in respect to actions taken based on any or all of the information on this writing.